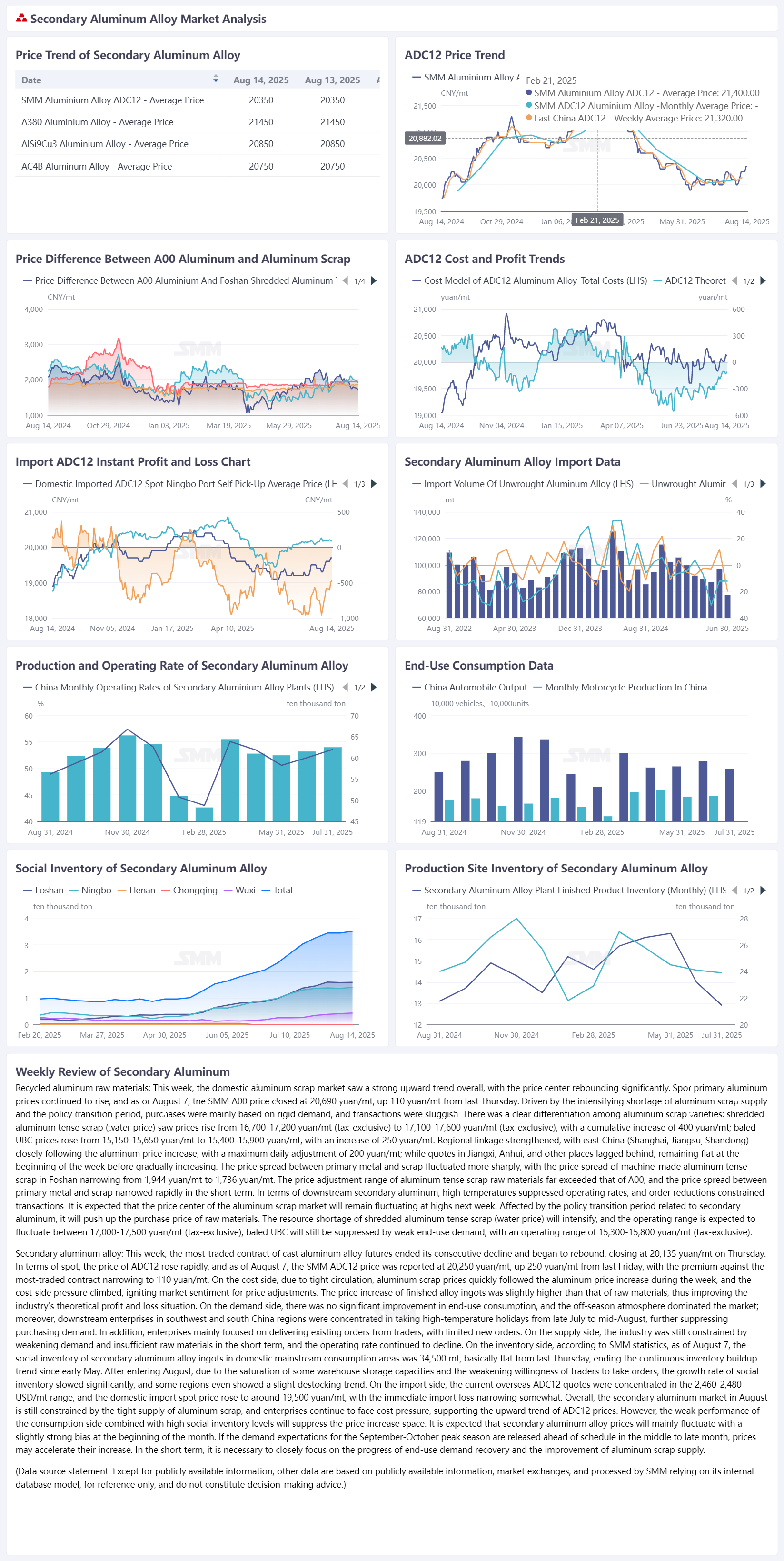

Recycled aluminum raw materials: The aluminum scrap market saw intensified supply tightness this week, with the price center moving upward again. As of August 14, the SMM A00 price closed at 20,710 yuan/mt, up 20 yuan/mt from Thursday last week. The intensified aluminum scrap supply shortage, coupled with the impact of the policy adjustment period, kept downstream purchases at just-in-time levels, with sluggish transactions. There was a clear differentiation among varieties: shredded aluminum tense scrap (with water content) saw prices rise from 17,000-17,500 yuan/mt to 17,100-17,600 yuan/mt (tax not included) at the beginning of the week due to difficulties in raw material purchases, while baled UBC prices increased from 15,400-15,900 yuan/mt to 15,500-16,000 yuan/mt, with a cumulative increase of 100 yuan/mt. Regional linkage strengthened, with the highest daily price increase of 200 yuan/mt in east China (Shanghai/Jiangsu/Shandong), while quotes in central China (Hubei) and other regions lagged behind. The price difference between primary metal and scrap continued to narrow, with the price difference between A00 aluminum and mixed aluminum extrusion scrap free of paint in Foshan compressing by 60 yuan/mt to 1,912 yuan/mt during the week. Downstream secondary aluminum enterprises were affected by the tight aluminum scrap supply and high temperatures that suppressed production, leading to high costs and weak orders. It is expected that the price center of the aluminum scrap market will move further upward next week. Affected by the policy adjustment period related to secondary aluminum, it will push up raw material purchase prices, with the supply of shredded aluminum tense scrap (with water content) remaining tight and the operating range expected to fluctuate between 17,100-17,600 yuan/mt (tax not included). Baled UBC, supported by downstream can stock enterprises' consumption, will operate within the range of 15,500-16,000 yuan/mt (tax not included).

Secondary aluminum alloy: This week, the most-traded contract of cast aluminum alloy futures fluctuated upward within the range of 20,050-20,300 yuan/mt, closing at 20,140 yuan/mt on Thursday. In the spot market, the price of ADC12 aluminum alloy increased slightly. As of August 14, the SMM ADC12 price was reported at 20,350 yuan/mt, up 100 yuan/mt from last Friday, with the premium against the most-traded contract expanding to 205 yuan/mt. On the cost side, considering the undersupply and potential policy adjustments, aluminum scrap prices followed the aluminum price increase rapidly. Meanwhile, the prices of auxiliary materials such as silicon and copper also edged up, further pushing up the cost of ADC12. As the price increase of finished alloy ingots outpaced the cost side, the industry's theoretical losses narrowed. Demand side, as August approaches its halfway point, the traditional off-season atmosphere in the market persists, with no significant improvement in actual consumption. Manufacturers and futures-to-spot traders face difficulties in selling, and transactions remain sluggish. In terms of supply, the overall operating rate of the industry shows a downward trend, mainly due to insufficient orders and losses. Additionally, some secondary aluminum enterprises recently reported that local governments are cleaning up and abolishing illegal fiscal rebates and incentive policies. Affected by this policy adjustment, some secondary aluminum plants have taken measures to reduce or suspend production to observe the subsequent implementation of the policies. On the inventory side, according to SMM statistics, as of August 14, the social inventory of secondary aluminum alloy ingots in major domestic consumption areas totaled 35,200 mt, an increase of 662 mt from last Thursday. As futures-to-spot traders' previous orders gradually entered warehouses and current consumption remains weak, the outflows from warehouses of alloy ingots are poor, and inventory continues to build up, albeit at a slower pace. In terms of imports, the current overseas quotes for ADC12 remain stable within the range of $2,460-2,480/mt, while the domestic import spot price has risen to around 19,700 yuan/mt. Coupled with the appreciation of the RMB, the immediate losses from imports have narrowed to within 500 yuan/mt. Short-term cost support and policy disruptions may continue to support the price to fluctuate upward, but weak demand and inventory buildup pressure will limit the upside room. Attention should be paid to the implementation of policies and the pace of demand recovery during the peak season.